‘True’ growth in OOH snacks and drinks as inflation releases its grip

There is clear evidence of real, organic growth in spend within the latest Kantar figures on the global out-of-home (OOH) snacks and non-alcoholic drinks market – driven by consumers making more trips. As price-per-unit has stabilised, the impact of inflation has reduced, with the price effect no longer the main catalyst for value increases. People have both the desire and the ability to increase their OOH consumption. At last, the clouds are parting.

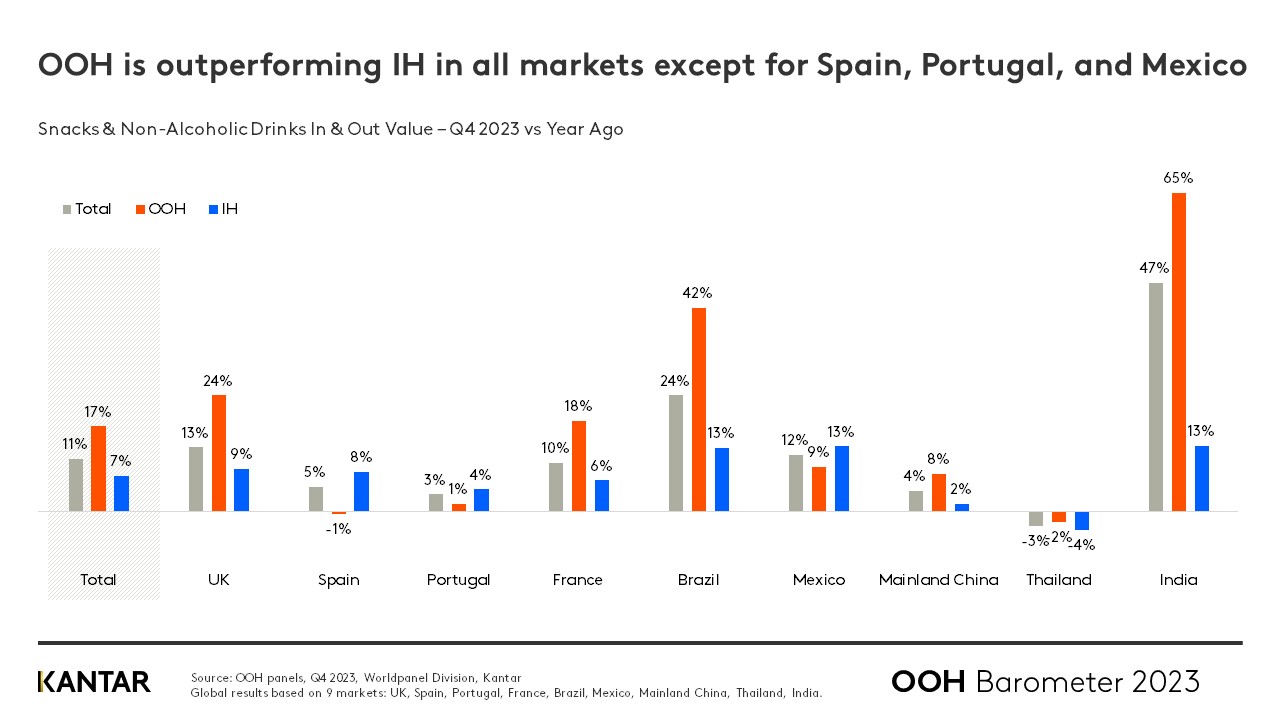

The total market for snacks and non-alcoholic drinks continues to grow at a steady rate across both in-home and out-of-home (OOH) occasions, with a combined value increase of 11% in the fourth quarter of 2023. Year-on-year OOH sales grew by 17%, outperforming in-home (7%); a trend we see in all markets except for Spain, Portugal and Mexico. The most significant increases came from India, Brazil and the UK.

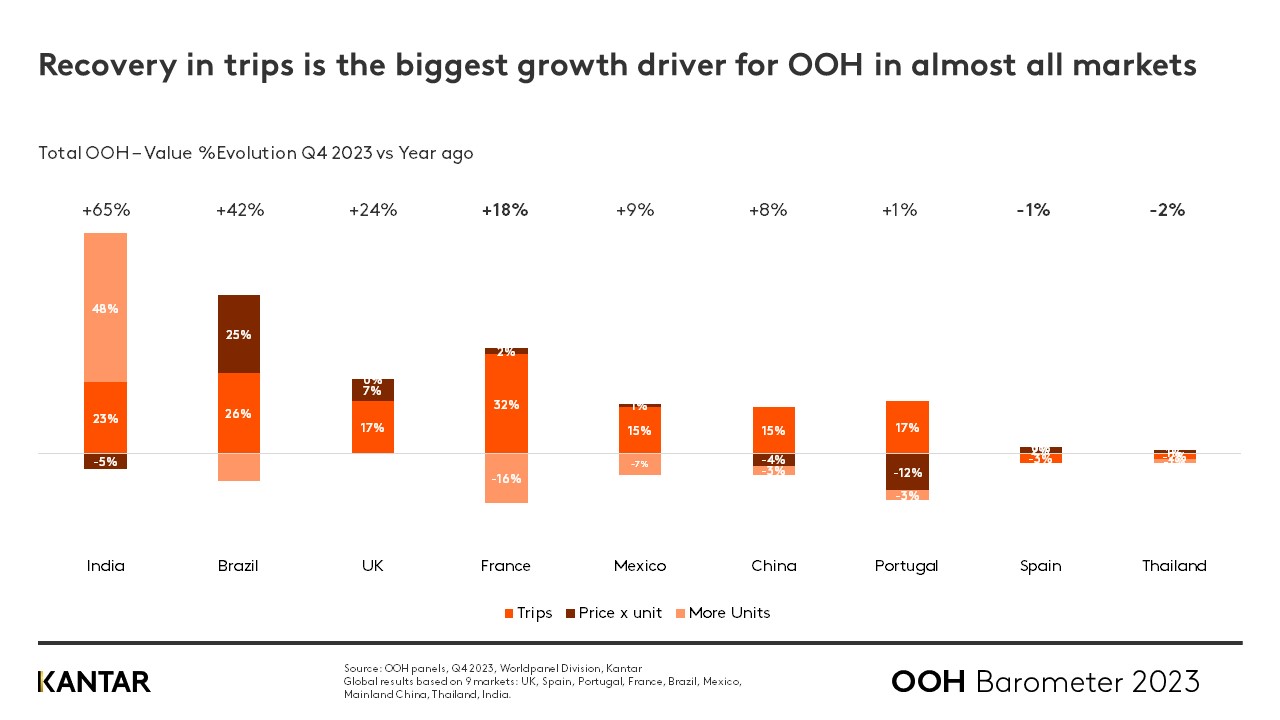

At a global level, consumers have increased the number of OOH trips they make by 16%, making this trend the main growth driver in almost all markets – in particular in Brazil, France and India. There was no uplift in Spain and Thailand, however, where the habit of consuming snacks and drinks OOH was already strong. Another reason for the lack of increase in frequency within those markets is that consumers are prioritising, and saving their money for special treats – such as visiting a restaurant at the weekend – rather than making smaller trips every day. This illustrates the importance of boosting routine trips to bars, cafes and impulse channels if the sector is to fully recover.

OOH value share continues to escalate

The OOH sector’s contribution to total spend on snacks and drinks has been rising consistently since 2021. Q4 of 2023 was no exception, with an increase in share from 35% to 37%. Only Spain and Portugal buck the trend, with higher spending on take-home consumption.

Impulse channels, bakeries, and traditional trade were the best performing OOH channels in Q4, with value share for snacks and drinks vs T.In&Out spend up 5.3%, 4.9% and 4.3% respectively compared to the same quarter the previous year.

Spotlight on snacks

Spend on snacking foods (+9%) is growing faster than either drinks (+5%) or meals (+7%), which is closely linked to the rising popularity of impulse channels, where people typically go to grab something quick to eat. This reinforces the rising trend for ‘on the go’ consumption we have tracked in previous quarters, and confirms the recovery of smaller, everyday OOH occasions.

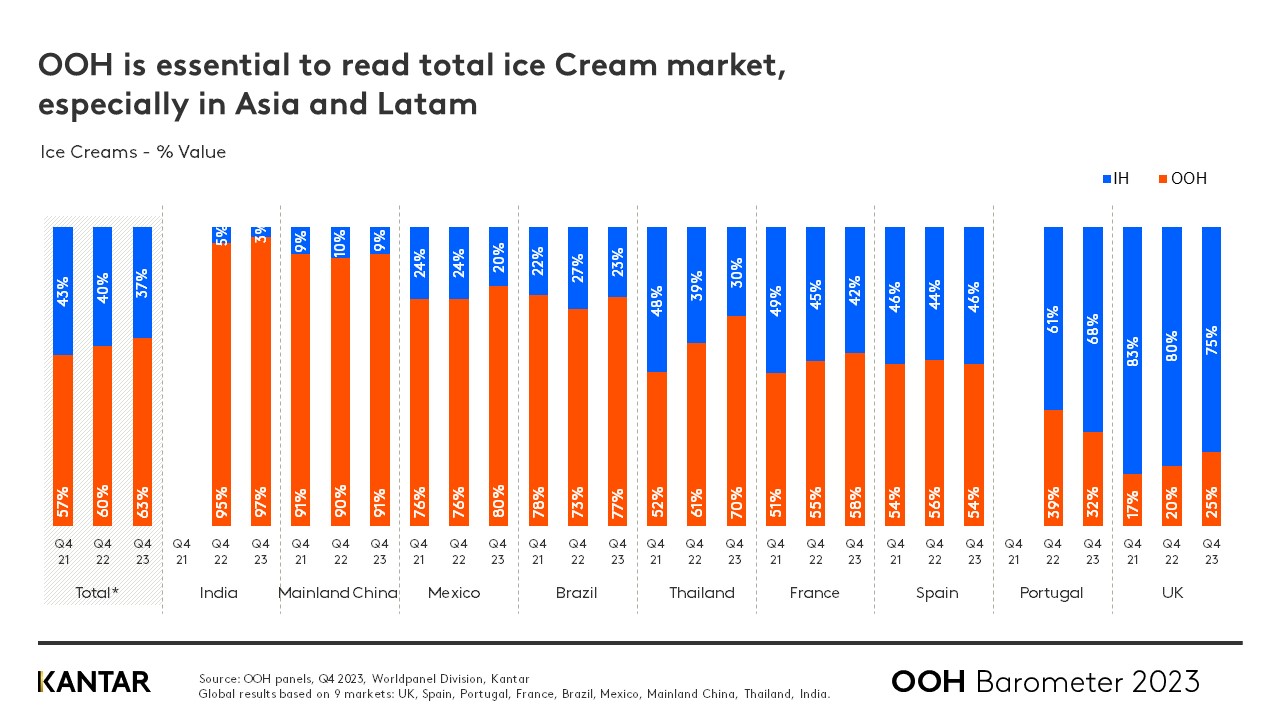

The ice cream and salty snacks categories grew most strongly in Q4 of 2023. This was a particularly remarkable feat for ice cream, considering that it was the winter season in many markets!

OOH occasions are vital to the performance of the ice cream category, contributing 63% of the total spend. This is especially true in Asia and Latam: in India 97% of all value is generated OOH, and the figure is 80% in Mexico. The proportion is lowest in the UK (25%). OOH ice cream sales are soaring in almost all markets, with the exception of Portugal and Thailand. The positive news is that the OOH growth has not come at the expense of in-home sales: spend is also growing in that environment.

Share of total ice cream spend vs T.In&Out is growing fastest in bakeries and other Horeca channels, including specialist ice cream shops (15.8%), together with impulse channels (8.9%).

Modern trade competes with QSR for meals

Switching focus from snacks to meals bought for immediate consumption, OOH again outperforms in-home in all markets apart from Spain, with value growth of 15% globally compared with 7% for in-home.

Growth is highest in Brazil (+38%) and Portugal (+19%).

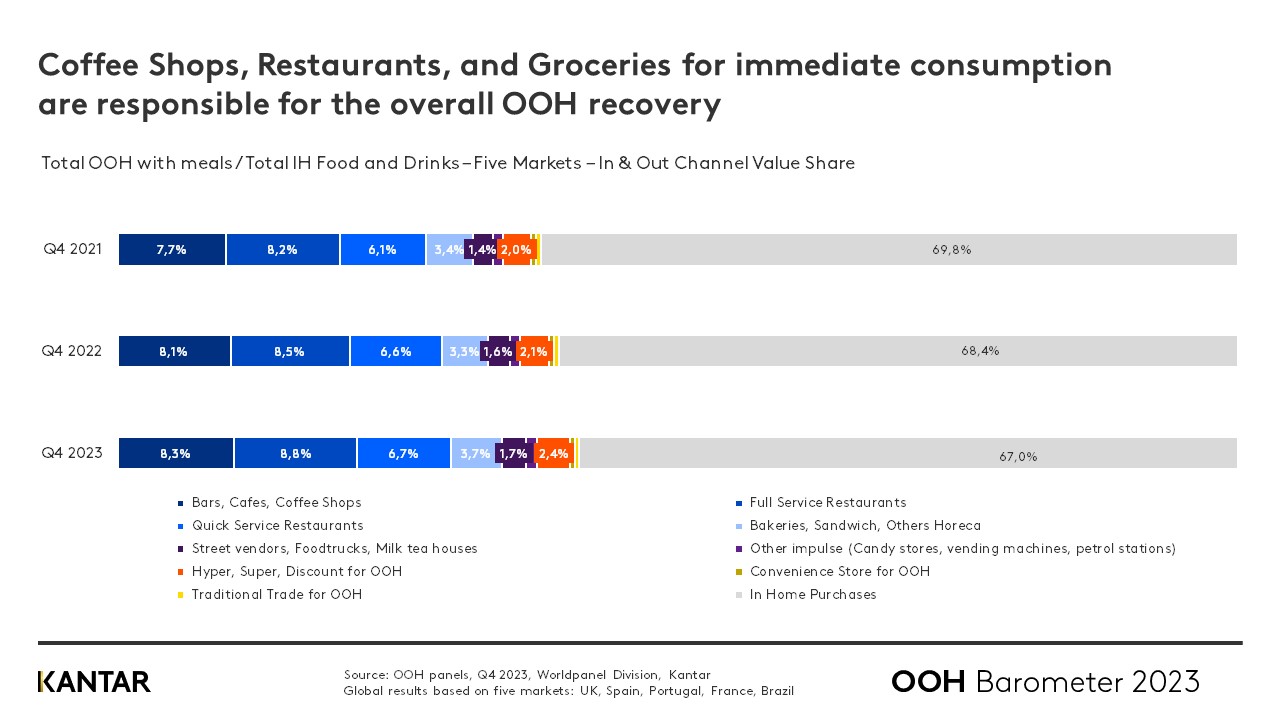

Coffee shops, restaurants and modern trade channels are responsible for this recovery. Supermarkets and hypermarkets that offer options such as hot food counters, sandwiches, sushi and salads have increased their market share to 2.4% – bringing them closer to quick service restaurants (QSR), which hold a 3.7% share. Modern trade is now competing directly with this channel.

--------------------------------------------------------------------------------------------